Retire In Peace (RIP) Portfolio Update

In my last post on this topic (https://www.valueforum.com/forums/show.mpl?keywords=1460037156.97.57&so=201604) I outlined an evolving strategy towards an income only portfolio designed to reduce/control trading induced by frequent online trading posts that we read every day.

There were a lot of useful comments. As expected, some disagreed with the strategy. I understand that & agree with many of the criticisms of a pure income portfolio - but this strategy has very specific goals in mind & I believe it will work just fine for me. It continues to evolve with my recent decision to favor AMT free municipal bonds for interest investments.

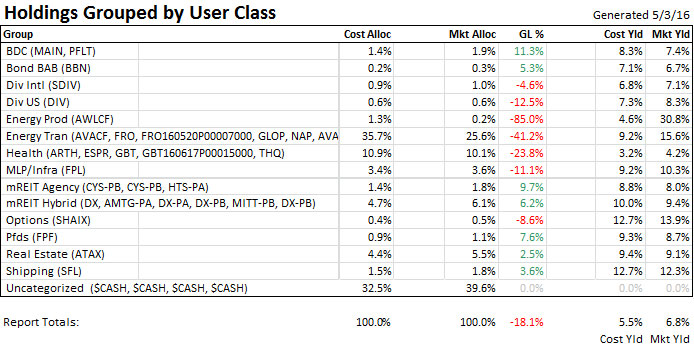

Here are the End Of April holdings in the 4 accounts using this strategy (other accounts are using TAA or are managed by an RIA). Not much has changed other than option expiration's. Legacy holdings (AWLCF, AVACF, FRO, GLOP, NAP) are cyclic and will remain until I’m ready to swap them for more appropriate income picks. Options will likely expire worthless. Spec Fliers (ARTH, ESPR, GBT) will remain at current levels until they are 10 baggers (I wish).

My main investment account has been gradually adopting this strategy (with the exception of the legacy stuff shown above) over the last few months and recorded a 4.3% gain in April.

Unfortunately, I can’t provide meaningful long term metrics since there has not been a well defined starting date for the strategy. It’s encouraging, however, to see the direction of the blue line reverse along with the gradual implementation. The fall of 2014 was devastating for previously discussed reasons (SDRL, NADL, etc).

In the last post I said I’d go over Bruce Miller’s strategy in more detail. That’s the focus of this post. This isn’t a book review. I’ll just try to explain the investment strategy as outlined by him. Miller expends a lot of space outlining how to select individual income stocks. I prefer ETFs & CEFs rather than the individual stocks because of my negative experiences with single company risk. There is no doubt that dividend funds such as DIV, SDIV, NOBL, SDY & VIG would be safer and easier to select and monitor than a portfolio of individual stocks. For this reason the RIP Portfolio will favor such funds. As it turns out, Miller is neutral on the topic and even goes to some length to point out the diversification advantages of mutual funds & ETFs.

Miller’s book covers the who, what, when, where, why & how of an income only portfolio. Every time I read through it I continue to find little pearls buried along with the maddeningly elementary (Chapter 3: “What exactly is a ‘Dividend’?”). This post will focus only on his method of selecting safe income producing individual stocks because it’s a useful learning experience in company analysis. If you want to learn more about the who, what, when, where & why you should buy the book: “Investing for Income ONLY” by Bruce F Miller, CFP. You can find the ebook on Amazon for only $4.49. (http://www.amazon.com/Retirement-Investing-Income-ONLY-Dividends-ebook/dp/B00O28ELH4).

On to Miller’s methodology...

The book’s premise is simple: he believes that, for many retirees, a pure income approach to investing is a better strategy than traditional total return Strategic Asset Allocation (SAA). Following his strategy requires ignoring market pricing as long as company fundamentals remain strong. The method can be psychologically difficult because inevitable market cycle corrections will be painful to ignore. “The paradigm of capital appreciation is deeply rooted, and many retirees, despite their thirst for long term reliable income, will not be willing to let it go. But as this book will make clear, letting it go is essential to successful income investing. No longer will the change in the price of an investment be the underlying force of investment decisions. Instead, the reliability and sustainability of the dividend will necessarily take its place.”

The beginning chapters go over standard financial planning to guide investor objectives. This includes determining the minimum required yield, income reliability, inflation protection, liquidity, capital preservation, estate planning and spells out his definition of income investing: “A method of selecting, purchasing and holding securities that pay reliable dividends, year after year, that cumulatively will provide the income the retirement household must have, throughout retirement”

According to Miller the advantage of this strategy is you can (1) ignore most market movements, (2) there is no need to fret over timing trades to generate income or rebalancing, (3) no need to spend time confirming you are on the right investment path (turn off MSNBC, and other opinionated - often wrong - information), (4) annual investment expenses are very close to zero (it’s all buy & hold with rare rebalance adjustments), (5) there is no requirement to deplete retirement savings (eg eat your seed corn), (6) there is no sense of urgency to take profits, (7) your death will not necessitate any significant portfolio changes for your survivors, (8) much of the portfolio’s income will be tax favored (although not all), (9) portfolio maintenance is easy and minimal once learned, and (10) most of the recommended investments grow dividends over time, eliminating the need to worry about inflation protection (except for fixed income).

There are, of course, some disadvantages. There is risk in that (1) he cannot provide any research or published information to verify the approach works, (2) the selected investments may slow their growth and reduce or eliminate dividends, (3) the screening and selection of securities requires considerable work, (4) inflation is a problem for any fixed income holdings and (5) your friends will think you are nuts.

A lot of time is spent defining terms that would be very familiar to VF members (dividends, interest, MLP, REITs, etc), so there is no reason to go over these parts of the book.

The meat of the book is the process of selecting and implementing an income only portfolio. Miller’s selection factors are as follows:

Yield: Figure out how much you can invest & how much you must earn from it. If you’ve got $500k of investable assets and need $25k of income to supplement your pension or SS then you’ll need to invest the $500k at an average yield of 5%

Dividend History: Find companies with a long history of paying dividends. He uses these sites

http://www.dripinvesting.org/ (downloadable, sortable spreadsheets)

http://www.longrundata.com/ (best for fast screening prospects found elsewhere)

to find these companies. He also charts the dividend history on his own so he can see the trend visually.

Examine Dividend Growth Rate looking for accelerating or decelerating dividend growth rates. For this he favors graphing his own dividend history and growth from yahoo’s data. The ideal income stock shows consistent dividend growth year after year - even during recessions. He also wants to avoid stocks that grow dividends too quickly, often indicating an unsustainable business practice. Slowing dividend growth often indicates a maturing business that may not continue to grow..

Nature of the investment’s business: It’s important to be comfortable with the company business model. A land-line telco or postage meter company (PBI) would probably not be a good investment when wireless & internet are stealing their market. Single product companies without a good “moat” are going to be at higher risk of competition with income loss as a result. Ethics also enters into this equation. Some may prefer to invest (or not) in tobacco or guns, for instance.

Dividend Coverage: Analyze financials to determine if the company can maintain its dividend. Miller notes that steps 5 & 6 are optional, but spends a lot of time outlining the methodology and recommends it. Basically, he uses Morningstar to look at quarterly Income Statements, Balance Sheets and Cash Flow on each company. From GAAP Revenue, Net Operating Cash Flow (Net OpCF), Investments (Net Cash Used for Investment Activities), Interest Expense, Dividends and Shareholder Equity values he determines the Interest portion of Net OpCF, Dividend portion of Net OpCF, annualized Revenue Growth and Net OpCF Growth to decide if the company is spending and earning enough to be able to continue paying dividends. (I’ll go over the detailed steps in the next post on this topic and introduce a custom spreadsheet to speed the evaluation)

Return on Invested Capital (ROIC): Income investors should favor companies that steadily raise their ROIC. These calculations are included in step 5 above.

Consider tax ramifications of 1099 Data (Ordinary vs Qualified vs LTCG vs STCG vs ROC vs Unrecaptured Sec 1250 gains, etc.)

Once the methodology is understood he goes over how to build the portfolio. There isn’t a lot of detail here because there is a lot of customization to each investor’s situation. Someone requiring a 6-7% dividend income will be forced to favor riskier investments (or maybe go back to work) whereas a 3% income requirement can be easily met with low risk securities.

A major point made throughout the book is that an income portfolio should be diversified for INCOME risk and not for MARKET risk. Reliable dividends are paid from cash flow, not earnings. Diversification between the various income groups is important. He does not place much value in metrics such as P/E, portfolio alpha, beta and so forth because these metrics are aimed at maximizing total return. His strategy is aimed at maximizing the probability that a dividend will be paid and grow over time.

Miller organizes security types into groups based on income risk, yield stability, tax treatment, growth & other factors. His method is aimed at reducing the risk that an investment will lower its distribution (and your income). As noted, he is not as concerned about the market risk - ie share price decline (although the two often go hand in hand). If the company’s fundamentals are sound the dividend should not change and the share price will return. A position is only sold when the fundamentals (ie cash flow necessary to support the dividend) deteriorates. We are advised to consider income risk when choosing investments. His Total Risk Score is the sum of his own subjective scoring of a group’s income risk from an (1) economic recession, (2) rising interest rates, (3) regulatory changes, (4) competition, (5) currency exchange rate changes and (6) product or service evolution. I show only the total scores in this reproduction of his income risk table (lower risk scores mean a lower risk the investment group will cut dividends). The complete table is on about page 189 (whatever that means in an ebook).

Income Group | Total Risk Score (Lower is better) | Ticker Examples |

Financials (banks) | 21 | BOH, WFC, JPM, CBKM |

Financials (Lenders, BDC) | 20 | MFI, TAXI, TCAP, WU |

Insurance | 14 | MET, ERIE, CNF, ORI |

Consumer Staples | 12 | CLX, PG, GIS, CPB, TIS |

Tobacco | 20 | MO, PM, RAI, LO |

Pharma | 18 | MRK, GSK, BMY |

Technology | 18 | CA, MSFT, INTC, ADP, ADI |

Telecom (US) | 16 | ENVE, T, CRL, VZ |

Telecom (foreign) | 19 | CHA, PHI, NTT |

Services | 14 | NTRI, TOO, TGP, SYY, WM, CLCT |

Industrials | 15 | PCL, PCH, WY, EMR, GE |

Energy/RT (Explore, Mine) | 14 | CVX, NE, XOM, VNR, HGT |

MLP (Midstream) | 13 | KMP/KMR, MMP, WMB, ETP |

MLP (Downstream, retail) | 16 | FGP, SGU, APU |

REIT (Retail, Business, Hosp, Apartments) | 13 | BXP, ARE, KIM, HW, LHO |

REIT (Medical, Storage) | 12 | HCP, OHI, HCN, LTC, NHI, PSA |

Utility (regulated) | 14 | PPL, ED, SO, POR, WEC |

Preferred Stock & Bonds | 7 | SUI-A, TCO-J, BGE-B, ARH-C |

He also provides a list of the Industries containing the most reliable dividend paying corporations:

Energy | Oil, gas, exploration, distribution |

Financial (banks) | Banks, lenders, financial services |

Insurance | Mostly to business |

Consumer staples non-cyclical | Beverages, footware, OTC meds |

Industry non-cyclical | Agriculture, business equip, chemical, waste |

Pharma | Manufacture & retail |

Tobacco | Domestic & Foreign |

Retail | Sales & distribution |

Tech | Manufacture & services |

Personal Services & Leisure | Hotel, vacation, gaming |

Medical | Equipment, services |

Aerospace, Defense | New products & long term service contracts |

His favored investment vehicles include:

Dividend paying C Corp common shares & their preferreds

Utility common shares & preferreds

Equity REITs. He favors healthcare & storage REITs for all markets. Business, Industrial, Retail, Residential & Hotel REITs are best during economic expansions and falter during contractions. He avoids mREITs because of volatility, high debt levels, & interest spread risks (he obviously doesn’t belong to VF or he would know about mREIT preferreds)

ETFs, OEFs & CEFs that avoid leverage

BDCs

Bonds (Corp, US Govt, Municipals)

Bond funds

MLPs in taxable accts only

Royalty Trusts

Exchange Traded Debt (Baby Bonds)

He avoids Unlisted REITs, ETNs, mREITs, Options, Unit Investment Trusts, Insurance company income products and Dividend capture investments

Miller’s diversification rules:

No more than 3% in an individual stock or MLP. So a portfolio of individual stocks should have a minimum of 34 holdings (less if ETFs or mutual funds are used)

No more than 20% in any one income group. A portfolio should include holdings in at least 5 income groups

No more than 20% in any single ETF, OEF or CEF. If an ETF is limited to one income group it should be included in the total holdings for that group

No more than 40% of the portfolio’s income should come from bonds or preferred stock of any one income group. So a portfolio of entirely bonds or preferreds should have bonds/preferreds from at least 3 income groups. Fewer income groups are allowed for bonds & preferreds because of their lower income risk.

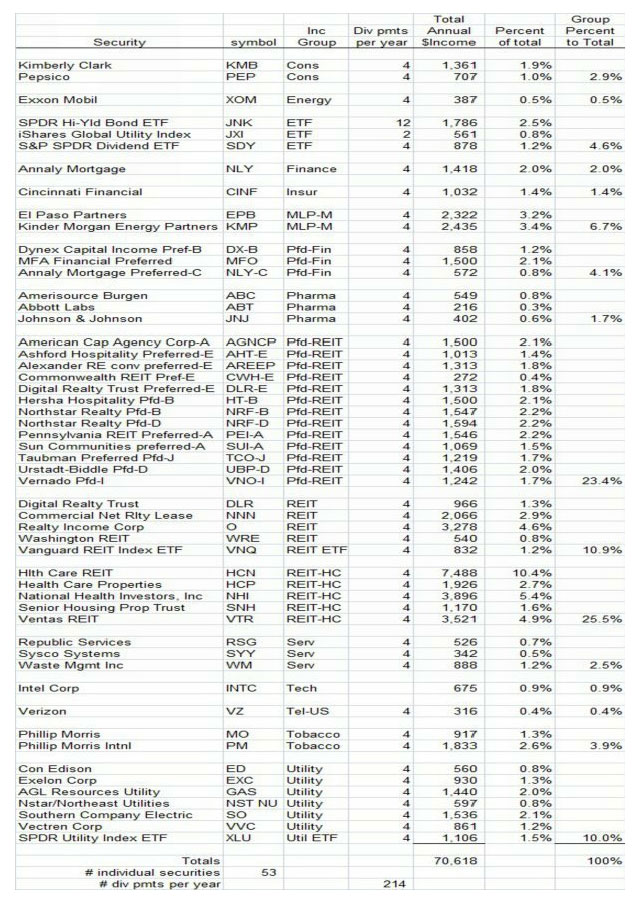

Page 192 includes an example of a portfolio built using the above rules. It contains a mixture of 53 individual stocks, preferreds and ETFs producing an income of 70k/year.

What is most important to Miller is the ability of his selected investments to continue paying distributions and to grow them over time. He believes his methods allow him to predict distribution stability and growth with some degree of confidence.

OK. That covers the Income Only strategy basics. My next post will go over the mechanics of selecting & analyzing one or two stock positions for an income only portfolio. I’ll include a spreadsheet that simplifies the analysis portion of the methodology.